Lately the media has been rife with articles about the new mortgage rules and how they impact the market. It has become obvious to most real estate junkies that the Toronto market has shifted from an intense seller’s market to a more balanced market.

These rules affect federally regulated lenders that fall under the OSFI umbrella (Office of the Superintendent of Financial Institutions), such as the banks (Scotiabank, Royal Bank, TD, BMO etc) and other institutions. Not all mortgage lenders are under the umbrella of OSFI such as provincial regulated Credit Unions. Therefore, it is important to know that as a borrower you have other options. The new mortgage rules pushed the lenders, under the OSFI umbrella, to be more cautious in areas such as background and credit checks on borrowers, document verification and property appraisals as well.

How do these changes impact you as a buyer and a seller? What should you do to protect yourself? How can you take advantage of the market slowdown?If you’re a buyer in today’s market, it is critical you speak with your mortgage broker and get an updated approval on the mortgage amount you qualify for under these new rules. Furthermore, it is imperative you understand that if you choose to overpay for a property because you “fell in love” then you may be at risk of the property not appraising for the price you paid. This would force you to come up with a higher down payment which you may or may not be able to do. We strongly recommend you submit your offer conditional on getting satisfactory financing AND conditional on the property appraising for what you paid. This way you will be able to walk away from the deal if your financing objectives have not been met.

If you’re a move up buyer in today’s market and are going to buy another house BEFORE you sell your current one, it is critical your real estate agent provide you with a market value for your current house that is conservative and not inflated. Otherwise, if you are counting on a dollar amount for your current house, you may be left with a financial shortfall compromising your ability to close on the house you bought. You may want to consider making the offer conditional on selling your current house but this may be met with resistance from sellers since the market is not a full blown buyer’s market. This strategy works best if you are considering making an offer on a house that has been languishing on the market with motivated sellers but it will not likely work on a property that has just been listed for sale.

Lately, we have seen many properties for sale by sellers that have bought another house and are anxiously trying to sell their current house. Most of these properties will sell because it is still an active real estate market. But some will undoubtedly sell for a lower price than the seller was expecting. This is not a pleasant position to be in as a seller.

So the strategies for buying and selling real estate today are not as straight forward as they were even a few weeks ago. The key is to be cautious, do your due diligence and hire a professional real estate agent whom you trust to give you the straight goods.

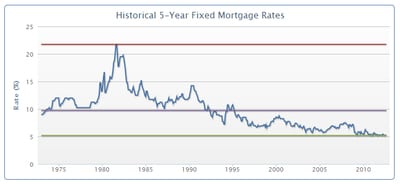

Overall it’s a great time for first time buyers with stable jobs to get into the real estate market especially if you are paying a high rent. Interest rates are at an all time low with some institutions offering a 5 year rate under 3% allowing you to make payments towards a mortgage rather than rent, building YOUR equity and not your landlords. Furthermore prices are softer that they were in the spring allowing you to buy a house without the stress that comes with an overly heated market.

If you’re a move up buyer looking to buy a bigger house, and have a stable job, this is an ideal time to buy up as well. The market is less frenzied than it has been all year potentially allowing you to negotiate rather than compete for a house. So although you may get less for your current house than you would have just a few months ago, you will pay less for the bigger house you want to buy as well. As we mentioned earlier, it is critical you take precaution to either sell your current house before buying a new one or use a conservative figure for what you expect to get from your current house in order to avoid a financial shortfall.

It is always our pleasure to assist you with your real estate needs. Please do not hesitate to call us for advice if you are not under contract with another brokerage.